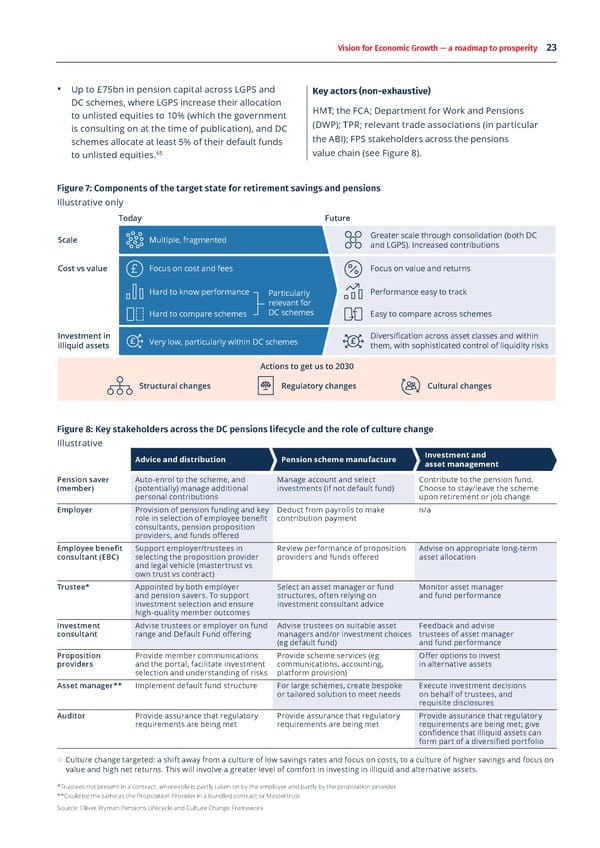

Vision for Economic Growth — a roadmap to prosperity 23 Big move #2 • Up to £75bn in pension capital across LGPS and Key actors (non-exhaustive) DC schemes, where LGPS increase their allocation HMT; the FCA; Department for Work and Pensions to unlisted equities to 10% (which the government (DWP); TPR; relevant trade associations (in particular Fully implement a programme of change is consulting on at the time of publication), and DC schemes allocate at least 5% of their default funds the ABI); FPS stakeholders across the pensions for UK pension and insurance funds 65 value chain (see Figure 8). to unlisted equities. In recent years, momentum has grown to strengthen consultants, and auditors. Change will require Figure 7: Components of the target state for retirement savings and pensions a sustained and broad-based campaign across capital markets and reform pensions. On capital markets, Illustrative only the Hill,55565758regulators and industry to help decision makers Kalifa, Austin, and Kent reviews proposed Today Future feel comfortable and con昀椀dent with the new strong steps forward. Many have been implemented, 59approach. Within some organisations, it may Greater scale through consolidation (both DC including through the Financial Services and Markets Act. ScaleMultiple, fragmented and LGPS). Increased contributions also require additional training or development They will have a signi昀椀cant impact on listings, secondary markets, and the equity research that underpins them. of specialist expertise to build comfort in investing Cost vs valueFocus on cost and feesFocus on value and returns But further work is critical to ensure that the UK is the in new asset classes. If new demand resulting from place where great companies can start, grow, scale this culture change cannot be met with new supply of Hard to know performanceParticularly Performance easy to track relevant for investment opportunities in the UK, then capital will and stay. This e昀昀ort is being taken forward by CMIT DC schemes Hard to compare schemes Easy to compare across schemes 昀氀ow overseas or remain in other, lower return, asset (the Capital Markets Industry Taskforce) as well as UK classes. So an even stronger pipeline of growth 昀椀rms Finance and TheCityUK. It is vital that their proposals Investment in Diversi昀椀cation across asset classes and within Very low, particularly within DC schemes will be vital which will require continued emphasis continue to receive strong support from government, illiquid assets them, with sophisticated control of liquidity risks 60 regulators and the industry.on seed and incubator capital being provided by Actions to get us to 2030 specialist early-stage investors encouraged by Pensions reform will also be critical to support improved 昀椀scal incentives.Structural changesRegulatory changes Cultural changes long-term returns for savers, as well as stronger capital • Make progress on reforms where there is strong markets and UK economic growth. The Mansion House 61and broad-ranging support. Particularly important Reforms propose potential changes to UK pensions. It will be important that proposals with widespread support will be implementing Solvency II reform and a new Figure 8: Key stakeholders across the DC pensions lifecycle and the role of culture change are followed through. Figure 7 provides an illustrative Value for Money (VFM) framework for DC schemes. Alongside these e昀昀orts is the Mansion House Compact, Illustrative summary of what some of the reforms seek to deliver.Advice and distribution Pension scheme manufacture Investment and a commitment by some of the UK’s largest pension asset management Changes to the legal framework are necessary. But 昀椀rms representing around two-thirds of the UKʼs Pension saver Auto-enrol to the scheme, and Manage account and select Contribute to the pension fund. it is cultural change around risk appetite, including entire DC workplace market to allocate a minimum (member)(potentially) manage additional investments (if not default fund)Choose to stay/leave the scheme personal contributions upon retirement or job change 63 investment in unlisted asset classes, that will ultimately of 5% of DC funds to unlisted equities by 2030. EmployerProvision of pension funding and key Deduct from payrolls to make n/a realise bene昀椀ts for savers, and the UK economy. The asset This will be complemented by large-scale investment contribution payment role in selection of employee bene昀椀t management industry will then need to make the most of consultants, pension proposition vehicles to deploy capital most e昀昀ectively. Scale will providers, and funds o昀昀ered these changes. The many stakeholders in DC pensions be critical. It will allow these funds to diversify broadly Review performance of proposition Advise on appropriate long-term that need to work together are outlined in Figure 8. A Employee bene昀椀t Support employer/trustees in consultant (EBC) selecting the proposition provider providers and funds o昀昀ered asset allocation and remain strongly involved throughout the scale- and legal vehicle (mastertrust vs good example of this approach in practice is on the long-up journey in later stage funding rounds. It will also own trust vs contract) term savings side, where regulatory reforms will allow — enable them to develop the world-class advice and Monitor asset manager Trustee* Appointed by both employer Select an asset manager or fund but not guarantee — greater infrastructure investment. structures, often relying on and fund performance and pension savers. To support experience needed by the companies they invest in, investment consultant advice The ABI’s Investment Delivery Forum supports 昀椀rms as investment selection and ensure comparable to that provided currently by US venture high-quality member outcomes they look at increasing allocations to assets such as capital 昀椀rms.Investment Advise trustees or employer on fund Advise trustees on suitable asset Feedback and advise 62 energy generation, energy networks and housing.consultantrange and Default Fund o昀昀eringmanagers and/or investment choices trustees of asset manager Benefits (eg default fund) and fund performance O昀昀er options to invest Proposition Provide member communications Provide scheme services (eg Key focus areas to deliver this target state are:Estimates indicate that there is a potential to unlock providersand the portal, facilitate investment communications, accounting, in alternative assets selection and understanding of risks platform provision) • Support cultural change across the investment billions in private capital from the insurance and long- Asset manager** Implement default fund structure For large schemes, create term savings industry by 2030: bespoke Execute investment decisions value chain, using regulatory and structural or tailored solution to meet needs on behalf of trustees, and changes and 昀椀nancial education as a key enabler. • Reforms to Solvency II could potentially unlock up to requisite disclosures The power to change capital deployment for pensions AuditorProvide assurance that regulatory Provide assurance that regulatory Provide assurance that regulatory £100bn from the insurance and long-term savings requirements are being met requirements are being met requirements are being met; give con昀椀dence that illiquid assets can sits right across the investment value chain. It starts industry into productive 昀椀nance, including for UK form part of a diversi昀椀ed portfolio with individual savers and employers and continues social infrastructure and green energy supply, over 64 through trustees, asset managers, employee bene昀椀t Culture change targeted: a shift away from a culture of low savings rates and focus on costs, to a culture of higher savings and focus on the decade from 2024.value and high net returns. This will involve a greater level of comfort in investing in illiquid and alternative assets. *Trustees not present in a contract, where role is partly taken on by the employer and partly by the proposition provider **Could be the same as the Proposition Provider in a bundled contract or Mastertrust Source: Oliver Wyman Pensions Lifecycle and Culture Change Framework

Vision for Economic Growth Page 22 Page 24

Vision for Economic Growth Page 22 Page 24