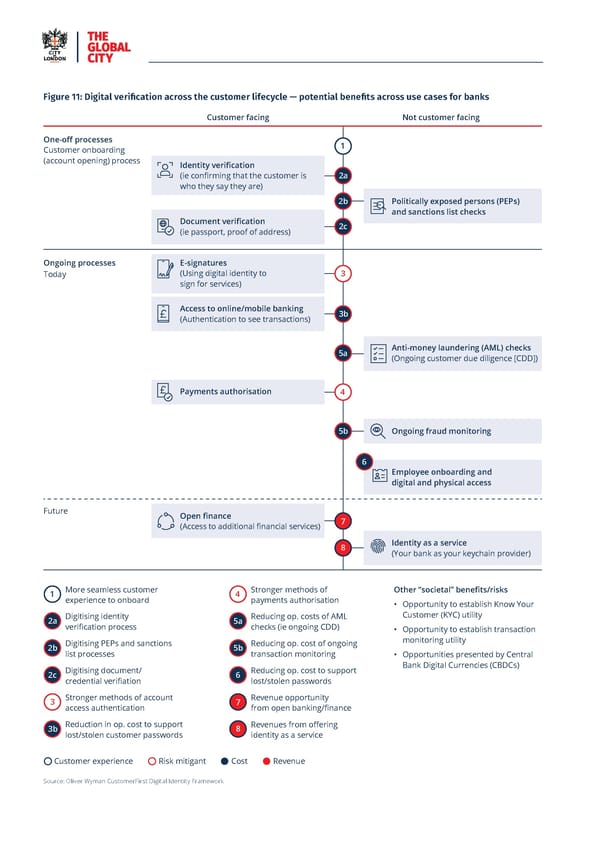

Vision for Economic Growth — a roadmap to prosperity 31 Figure 11: Digital verification across the customer lifecycle — potential benefits across use cases for banks Big move #5 Customer facing Not customer facing Invest in driving an innovation and growth mindset One-off processes 1 Customer onboarding (account opening) process Implementing a digital-昀椀rst economy requires • Task regulators with deploying machine-readable Identity veri昀椀cation 2a (ie con昀椀rming that the customer is government, regulators, and the industry to all play a and machine-executable regulation, building on who they say they are) part. Regulators will need to further invest in their people, efforts underway by the FCA and the BoE. Machine- 2b Politically exposed persons (PEPs) systems, and technologies to keep pace with competing readable regulation (MRR) and machine-executable and sanctions list checks jurisdictions. They will also need to work together and regulation (MER) translate regulation into computer Document veri昀椀cation 2c provide global leadership on interoperable standards code such that compliance requirements can be (ie passport, proof of address) for emerging technologies (see Chapter 5). For the FCA managed in an automated way. This, in turn, will Ongoing processes E-signatures and the PRA speci昀椀cally, this will help to deliver on their reduce the compliance burden on 昀椀rms which can Today (Using digital identity to 3 secondary international competitiveness and growth then allocate more capital to innovation activities. sign for services) objective. The key actions to realise this big move are: Equally it will allow supervisors to be more agile and • Enable regulators to provide collective leadership strategic. They will be able to focus less on process and assembling data, more on addressing risks. MRR Access to online/mobile banking 3b on cross-sectoral priorities such as digital (Authentication to see transactions) veri昀椀cation, data, tokenisation and AI. The digital can also free up capacity, enabling supervisors to assess new risks and opportunities from emerging transformations of the next few years will require technologies. Today, these emerging technologies 5a Anti-money laundering (AML) checks agile, coherent responses. There will need to be (Ongoing customer due diligence [CDD]) a consistent approach across the regulators on include tokenisation and generative AI. They may look emerging technologies. Their role will be critical if we di昀昀erent in a few years’ time. Continued investment Payments authorisation 4 into innovative technology and 昀椀nancial supervision are to implement digital veri昀椀cation, manage data, (SupTech) to automate supervisory processes and and maximise the positive impact of AI. Fortunately, enable real-time monitoring of key risk indicators the DRCF is already working across silos more 91 5b Ongoing fraud monitoring and early warning signs will therefore be critical. e昀昀ectively. It should be given appropriate resources E昀昀orts should build on the FCA’s and BoE’s pilots on and an even stronger mandate to drive regulatory coordination for digital issues. It would focus both digital regulatory reporting, which explore automating 6 and streamlining various aspects of the regulatory Employee onboarding and on strategic outcomes and operational e昀漀ciency, 92 digital and physical access aligning reporting requirements across regulators. reporting process. • Streamline approaches to creating regulatory Benefits Future reform. The UK must continue to take pride in high Open 昀椀nance 7 This move will serve as a key enabler for innovation (Access to additional 昀椀nancial services) regulatory standards. But there is an opportunity to across the UK, and also support delivery of some 8 Identity as a service consider how the existing months-long approaches cornerstone innovations such as digital veri昀椀cation, (Your bank as your keychain provider) of consultation and creation of discussion papers can be complemented with more “agile” approaches, the bene昀椀ts of which are estimated for illustrative purposes in the previous move. whereby industry feedback is captured “live.” Stronger methods of More seamless customer Other “societal” bene昀椀ts/risks 1 experience to onboard 4 payments authorisation One recommendation could be to capture these • Opportunity to establish Know Your Key actors (non-exhaustive) ideas through a public-private partnership forum, Digitising identity Reducing op. costs of AML Customer (KYC) utility potentially as part of the FPS Partnership Council 2a 5a checks (ie ongoing CDD) DRCF members (ICO, CMA, FCA, OfCom); DSIT; Cabinet veri昀椀cation process • Opportunity to establish transaction (see Big move #1), tasked with testing very speci昀椀c monitoring utility O昀漀ce; Parliament; other 昀椀nancial services regulators 2b Digitising PEPs and sanctions 5b Reducing op. cost of ongoing areas or topics where regulatory reform might (see Figure 4). list processes transaction monitoring • Opportunities presented by Central be required. Digitising document/ Reducing op. cost to support Bank Digital Currencies (CBDCs) 2c 6 lost/stolen passwords credential veri昀椀ation 3 Stronger methods of account 7 Revenue opportunity access authentication from open banking/昀椀nance Reduction in op. cost to support 3b 8 Revenues from o昀昀ering lost/stolen customer passwords identity as a service Customer experience Risk mitigant Cost Revenue Source: Oliver Wyman CustomerFirst Digital Identity Framework

Vision for Economic Growth Page 29 Page 31

Vision for Economic Growth Page 29 Page 31