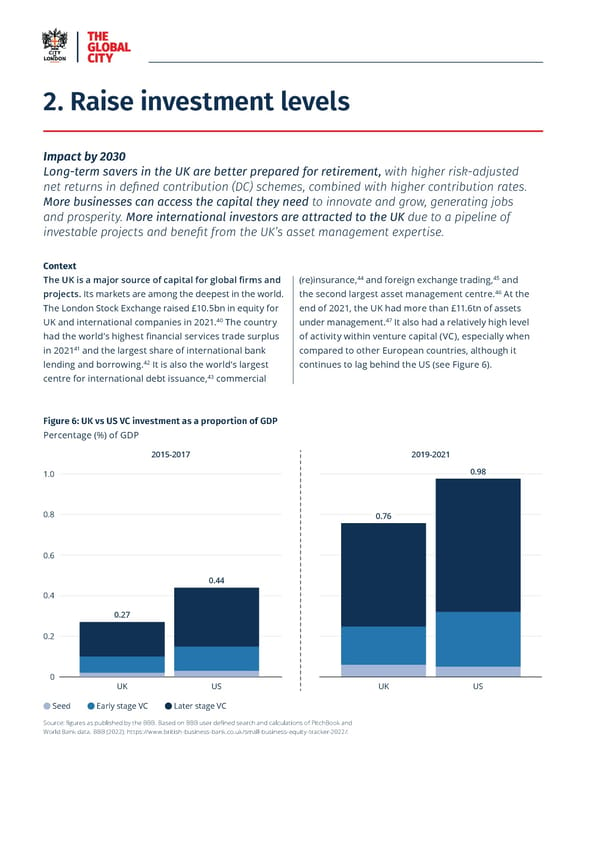

Vision for Economic Growth — a roadmap to prosperity 21 2. Raise investment levels Impact by 2030 Long-term savers in the UK are better prepared for retirement, with higher risk-adjusted net returns in defined contribution (DC) schemes, combined with higher contribution rates. More businesses can access the capital they need to innovate and grow, generating jobs and prosperity. More international investors are attracted to the UK due to a pipeline of investable projects and benefit from the UK’s asset management expertise. Context 44 45 (re)insurance, and foreign exchange trading, and The UK is a major source of capital for global 昀椀rms and 46 projects. Its markets are among the deepest in the world. the second largest asset management centre. At the end of 2021, the UK had more than £11.6tn of assets The London Stock Exchange raised £10.5bn in equity for 40 47 UK and international companies in 2021. The country under management. It also had a relatively high level had the world’s highest 昀椀nancial services trade surplus of activity within venture capital (VC), especially when 41 and the largest share of international bank in 2021 compared to other European countries, although it 42 lending and borrowing. It is also the world’s largest continues to lag behind the US (see Figure 6). 43 centre for international debt issuance, commercial Figure 6: UK vs US VC investment as a proportion of GDP Percentage (%) of GDP 2015-2017 2019-2021 1.0 0.98 Today’s domestic capital pools are not maximised UK. As of 2021, there were more than 15 times as many for UK savers, nor the broader UK economy. The savers accumulating in DC schemes than accumulating 0.8 0.76 51 There is also an estimated 35% gender overriding purpose of pension schemes is to pay savers in DB schemes. an income in their retirement. Insurance funds also pension gap across DB and DC schemes, with men 52 having more in savings. 0.6 have a key role to play in supporting long-term savers. Where this goal aligns with risk-adjusted net returns, Better returns on DC savings schemes could 0.44 there is signi昀椀cant opportunity to unlock capital to fuel begin to 昀椀ll part of the long-term savings gap 0.4 economic growth. UK pension funds have the highest allocation to bonds and lowest allocation to equities for pension savers. Analysis by Oliver Wyman and 0.27 48 of any comparable pension system in the world. the British Business Bank suggests that if default 0.2 They also have lower contribution rates by employers funds followed a lifestyle approach and allocated and employees alike. In 2019, employers on average 5% of capital to VC or Growth Equity (GE), a 22-year- contributed to de昀椀ned bene昀椀t (DB) schemes at a rate 6 old saver could achieve up to 12% increase in their total 49 53 Beyond bene昀椀ts to long-term times higher than to de昀椀ned contribution (DC) schemes. 0 retirement savings. UK US UK US DC savers are also, generally, not contributing enough to savers, the UK’s high-growth businesses would also Seed Early stage VC Later stage VC their pension schemes. As of 2019, 53% of private sector bene昀椀t if a proportion of these investments were pension participants across schemes had contributions allocated to UK businesses. The BBB estimates that Source: 昀椀gures as published by the BBB. Based on BBB user de昀椀ned search and calculations of PitchBook and World Bank data. BBB (2022): https://www.british-business-bank.co.uk/small-business-equity-tracker-2022/. 50 Collectively, these of less than 8% of their earnings. barriers to 昀椀nance could be preventing up to 270,000 dynamics mean that most DC schemes are inadequate for small and medium-sized enterprises (SMEs) from 54 More capital could therefore providing a comfortable retirement. This is signi昀椀cant innovating every year. help to encourage more innovation across the country. given the role that DC schemes play and will play in the

Vision for Economic Growth Page 19 Page 21

Vision for Economic Growth Page 19 Page 21